2 Undervalued Software Stocks to Buy Now: Figma and Industry Giants

The recent software sector sell-off has created a rare opportunity to buy high-quality companies at a discount. Explore why Figma and other undervalued giants are currently a steal despite the market panic over AI.

For many investors, 2026 began with major fears of the bursting of a massive tech and AI bubble. While a correction is finally materializing on the stock market, it is taking an unexpected turn: the creators of artificial intelligence remain relatively stable, while the traditional software sector is facing a brutal sell-off.

The prevailing anxiety that AI will completely cannibalize traditional software has triggered a massive wave of panic selling, pushing high-quality companies to valuation levels that many analysts consider irrationally low.

The Tech Sector Sell-Off: Software Under Fire

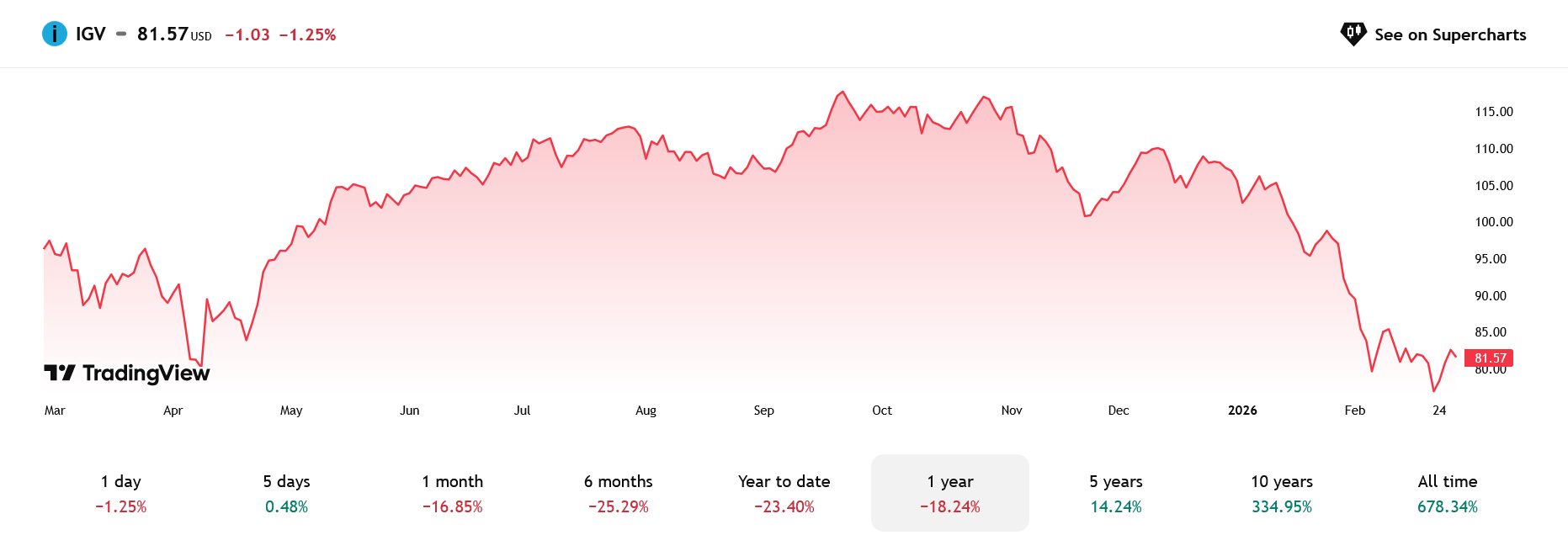

The impact of this shift is most visible in the iShares Expanded Tech-Software Sector ETF, which has surrendered more than 25% of its value in just the last six months. This "indiscriminate" selling has hit everyone from high-growth startups to established tech titans.

Even industry giants like Microsoft, Palantir, and the historically stable Salesforce have not been immune to this sudden shift in market sentiment.

While some price corrections were arguably necessary for overvalued stocks, the current "punishment" of the entire sector has created a unique opportunity to acquire great companies with healthy fundamentals at a discount. Two specific cases—Figma and Axon Enterprise—stand out as prime examples of where market panic has potentially decoupled from business reality.

1. Figma: A Rollercoaster Ride from Euphoria to Overselling

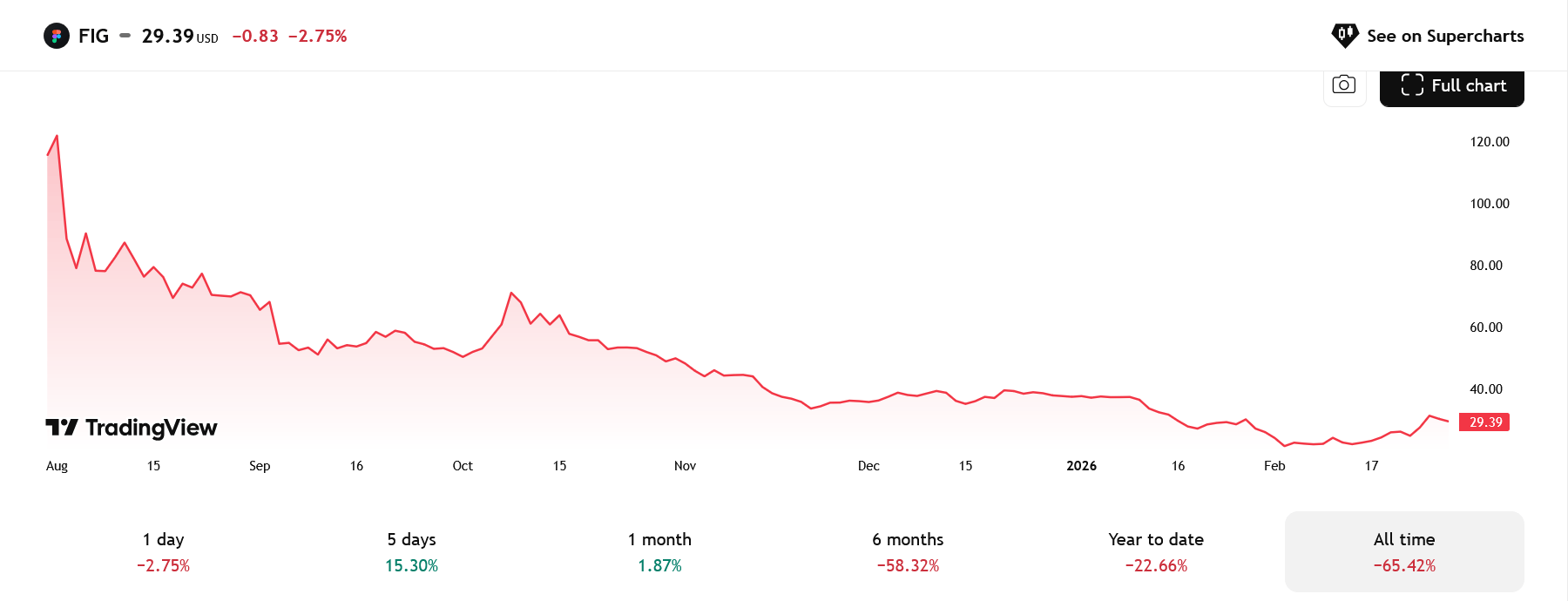

The journey of the design platform Figma over the last seven months has been nothing short of volatile. Following its highly anticipated IPO in July 2025, the company became the poster child for market enthusiasm.

- The Peak: Opening at $85, shares shot to $115 on the first day—marking the most successful first-day performance in the U.S. markets in three decades.

- The Fall: A painful descent followed, bottoming out near the $30 mark—a staggering 74% decline from its all-time high.

- The Valuation Gap: Market capitalization shrank to $10 billion, notably half of what Adobe was willing to pay in its blocked 2022 acquisition attempt.

Financial Resilience Amidst the Noise

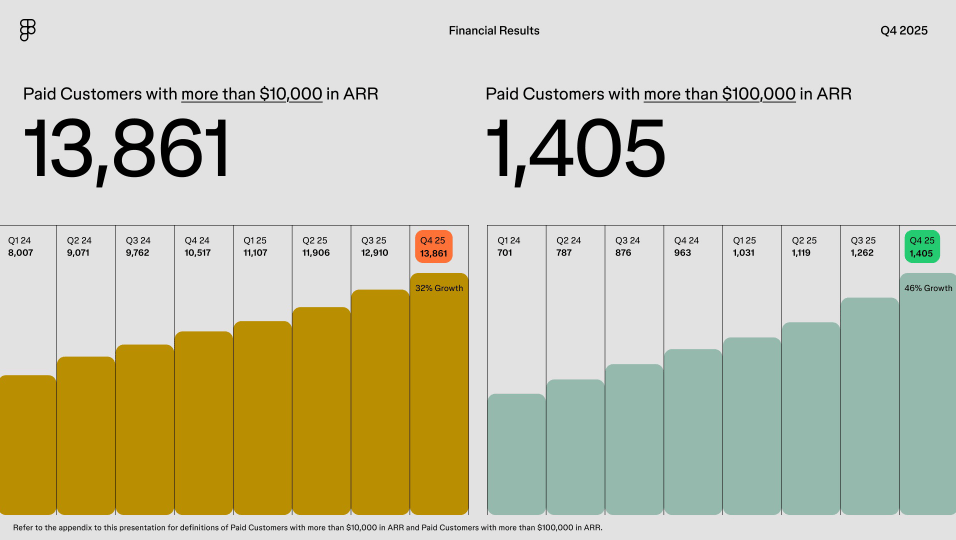

Despite the stock price carnage, Figma’s business fundamentals remain robust. The drop reflects a return to market reality rather than a collapse of the business model. In Q4 2026, Figma reported:

- Revenue Growth: A 40% year-over-year increase to $304 million.

- Milestone: Full-year turnover successfully surpassed the $1 billion mark.

- Retention: A net revenue retention rate of 136%, proving that existing users are consistently increasing their spending.

AI: Existential Threat or Strategic Asset?

Figma’s strategy suggests that AI is a tailwind rather than a headwind. By integrating AI tools like Figma Make, the company saw a 70% growth in weekly active users. Strategic partnerships with Anthropic and integrations with ChatGPT reinforce its position as an innovator.

Starting March 2024, Figma is implementing a credit-based monetization model for AI features, directly turning smart assistance into a new revenue stream.

2. Axon Enterprise: When Hardware Acts as a Shield

Axon Enterprise—the undisputed leader in public safety technology—is perhaps the most misunderstood victim of the software sell-off. Known for its Tasers, body cameras, and evidence management software, its stock price recently plummeted by 50%.

“Investors panicking over SaaS weakness have mistakenly thrown Axon into the same category, ignoring the company’s essential physical hardware component.”

From a high of $871 in August, the stock crashed alongside pure software plays. However, the logic that AI will replace Axon's products fails to account for the physical nature of law enforcement.

The "Moat" of Mixed Reality and Physicality

Axon’s business is protected by a multi-layered moat:

- Hardware Dependency: Taser sales grew 32% in Q4, accounting for a third of revenue. AI cannot physically restrain a suspect.

- Ecosystem Lock-in: Body cameras are linked to a proprietary secure platform. Replacing this would require a massive overhead in retraining and data migration for police forces.

- AI Integration: Tools like Draft One use AI to automate police reports from audio recordings, actually increasing the value of their software suite.

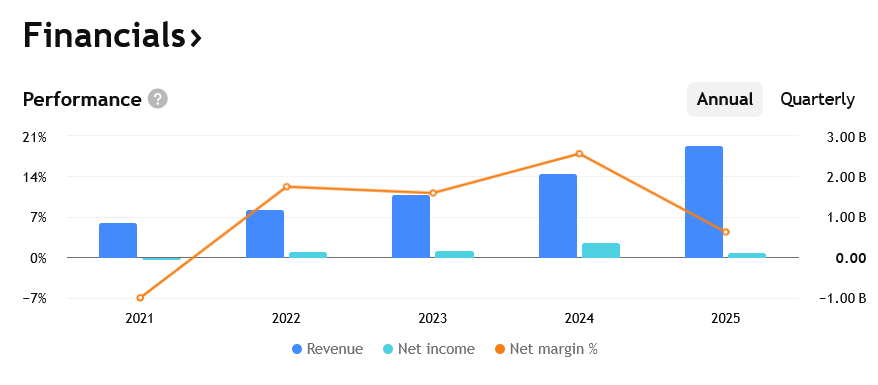

Stunning Financial Results

While the market panicked, Axon’s numbers told a different story. Quarterly revenue grew 39% to $797 million, while EBITDA profitability surged by 46% to $206 million. Most importantly, the company sits on $14.4 billion in binding future orders.

Summary: Market Irrationality Provides Entry Points

The recent rebound in Axon’s shares (up 18% following their earnings report) suggests that the market is beginning to wake up to its mistake. With management targeting $6 billion in annual revenue by 2028, the gap between perceived risk and actual performance remains a key focus for observant investors.